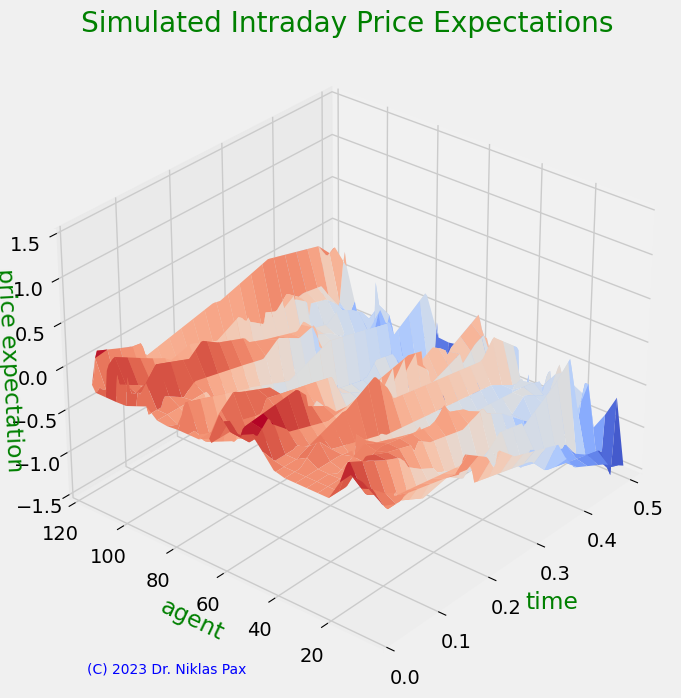

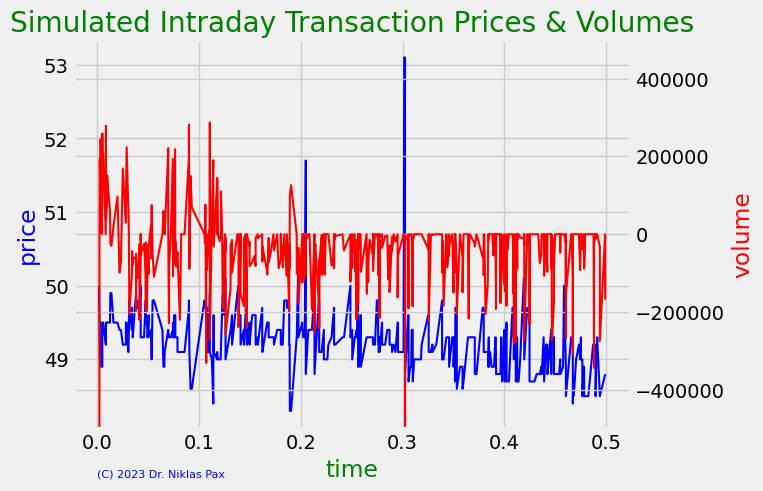

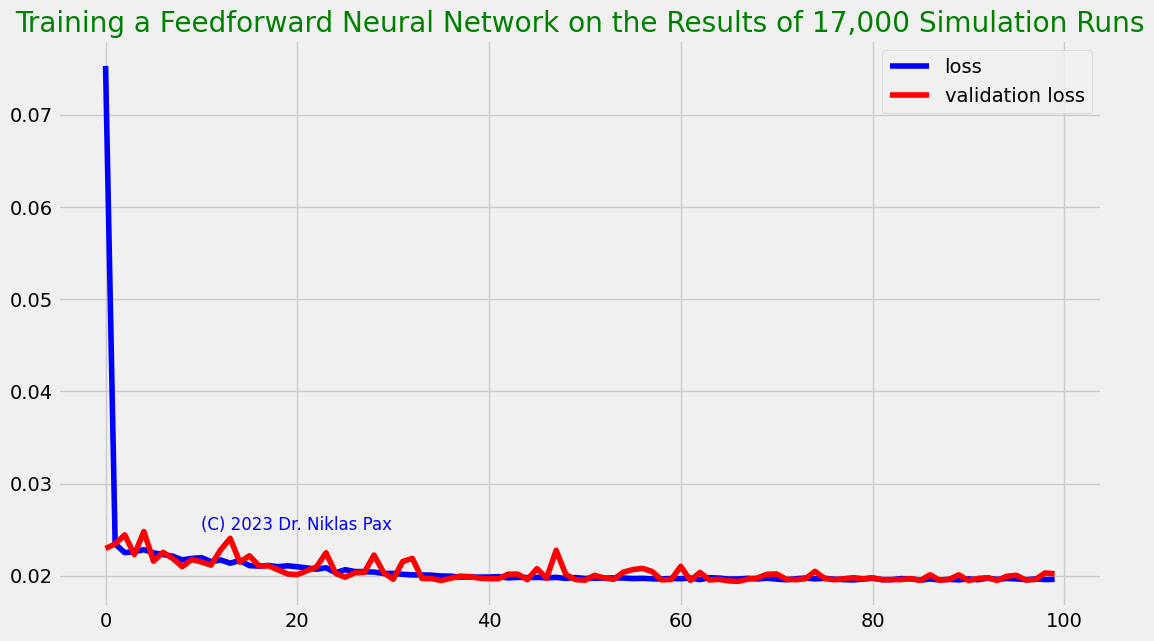

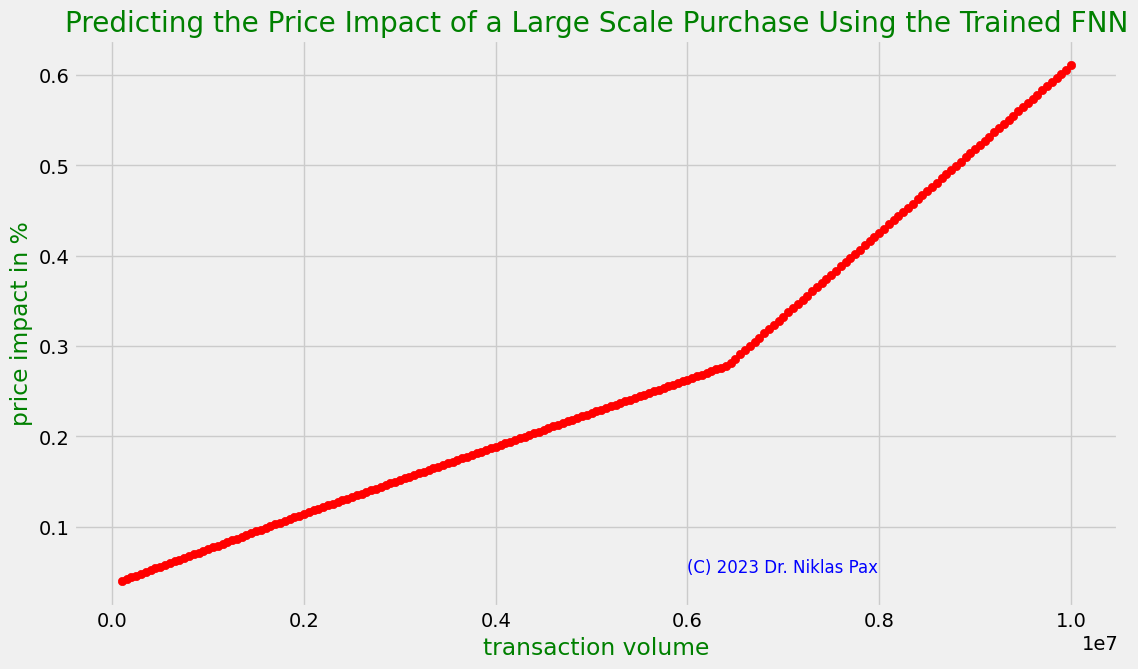

Building a Price Impact Model for Securities Transactions Using Deep Learning and Agent Based Modelling

Estimating the price impact of a large scale stock purchase using a feedforward neural network trained on the results of intraday data generated by agent based modelling (catallactics, cf. https://www.wu.ac.at/fileadmin/wu/d/i/finance/wissenschaftlMitarbeiter/Loistl_Otto/Bilder-Dateien/ci.pdf)